|

|

|

|

|

|

Ghosts of the Future

Dear Friends,

by Loren Cobb

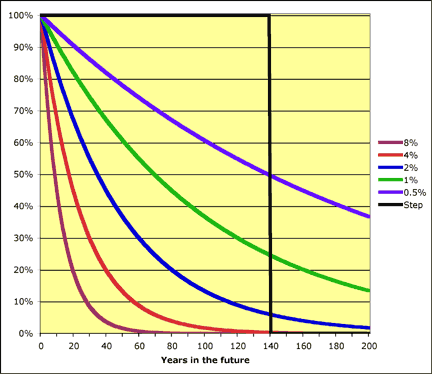

The news these days is filled with intimations of catastrophe. Will the approaching decline in worldwide petroleum reserves cause wars and famine? Have we caused global warming, and if so, will we suffer unimaginable climate change? These are just two of the ghosts that haunt our misty visions of the future. Earlier generations had their own ghosts. Most of us can well remember the fear of nuclear holocaust, and I have often thought about that dark period from about 1940 to 1942, when it must have seemed to any rational observer that all of civilization was about to destroy itself. Looking into the deep future, astrophysicists predict that our sun will someday turn into a red giant not unlike Betelgeuse, the huge red star on Orion's left shoulder. When this happens its diameter will rapidly expand out beyond the orbit of the Earth, utterly incinerating our entire planet. Fortunately this disaster lies some five billion years in the future, so few people stay up at night worrying about it. How can we weigh all of the factors describing an anticipated future disaster, to determine what is worth worrying about? How do we balance the size of a potential disaster against its depth in the future and the certainty of our knowledge? These are questions we can answer, concluding with a troubling example: the potential disruption of the oceanic currents due to global warming. The Value of Future Benefits and CostsIf you had the choice, would you rather receive a gift of $100,000 right now, or $10,000 every year for fifteen years? Questions like this have tortured the minds of lottery winners ever since delayed pay-out options were first introduced. (Would that we all may face dilemmas such as this.) Fortunately, there is a well-accepted method for assigning progressively less desirability to payoffs increasingly far in the future. This technique, known as discounting the future, was touched upon in TQE 136, last year. Part of the magic of discounting the future is that a wide variety of personal preferences can be described by just one simple parameter, the discount rate. The graph below shows how sharply events in the future are discounted, based on the discount rate. Five curves are shown, corresponding to discount rates ranging from 8% down to 0.5%. A high discount rate means that we strongly discount the future, and pay most attention to what is about to happen right now. If the rate is 8%, for example (the plum-colored curve) then events 60 years in the future receive almost no weight.

A low discount rate means that we prefer to take remote events into account as well. At a discount rate of 0.5% (the purple curve), events even two centuries in the future still have significant weight. For comparison, I have also included the system implied by that perennial favorite of environmentalists, a quote from the Great Law of the Iroquois: "In our every deliberation we must consider the impact of our decisions on the next seven generations." This is the black curve, according to which we should give full weight to any event occurring up to 140 years in the future, and then no weight at all to anything that occurs thereafter. Note that the black curve is almost the mirror image of the plum-colored high discount curve. The present value of a future benefit is simply its face value multiplied by the appropriate discount, which depends on the discount rate and how long we have to wait before receiving the benefit. The net present value of a series of benefits and costs is just the sum of all discounted benefits and costs. When financial analysts assess a business investment, they compare its initial cost to the net present value of all of its future returns and costs. If the initial cost is higher than its net present value, then it looks like a very bad investment. The same can be done for government policy decisions: compare the initial cost of implementing the policy to the net present value of all of its future benefits and costs. In the business world, the natural choice for a discount rate is the cost of obtaining capital, i.e. the interest rate charged by a bank for a business loan (I am ignoring equity capital here for the sake of simplicity). Any other rate, higher or lower, will result in sub-optimal business decisions which give the competition an advantage. A corporation that cannot properly evaluate the net present value of an investment will not long survive. Environmentalists tend to favor very low discount rates, reflecting the very slow rate of genetic adaptation in biological communities, whereas everything in a businessman's experience and training tells him that he should set the discount rate equal to the cost of capital. This is one crucial reason why capitalists and environmentalists are so often at terrible odds with each other. The Effect of UncertaintyFor most of us, the deeper into the future we try to peer, the more uncertain are the events that we so dimly perceive. Surely this uncertainty must affect the way in which we compare strategic courses of action? It would seem so, and yet the "net present value" calculation as shown above assumes perfect certainty with respect to the timing and size of future costs and benefits. Something is missing.

Suppose you have just bought a newspaper and a ticket for next week's million-dollar lottery. Then you read the newspaper and learn that the odds of winning are one in ten million. How much is your ticket worth? The expected value of your lottery ticket is the payoff times the probability: just ten lousy cents. If you play this lottery repeatedly, then this will be your average income per play. In general, if probabilities can be sensibly defined for a future benefit, then to find the expected value of the benefit just multiply the value of the benefit by its probability*. If you paid a dollar for the ticket, then some would say that it was a bad investment. Opinions differ sharply on this point, because not everyone tries to optimize expected value. People who for reasons of poverty wish instead to secure the mere possibility of wealth, no matter how improbable, will happily buy lottery tickets. If the possible benefit is to arrive in the future, then we need to discount its value to the present. In other words, we need to think about its expected present value. In simplest possible terms, to calculate an expected present value of a future benefit we simply multiply the present value by its probability*. Now suppose that there are a range of possible benefits, each with an associated probability. In this case we multiply each possible discounted benefit by its probability, and add up the results. The sum is the expected present value of the entire range of possible benefits. Similarly, when there are possible costs as well as benefits in the future, then the sum of all of the expected discounted values, positive and negative, is called the expected net present value.

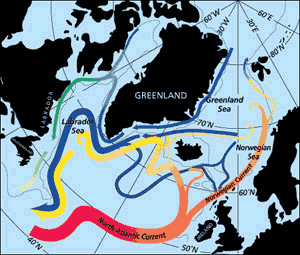

An Application: Europe in the Deep FreezeIn 2003, the Pentagon produced a shocking 25-year scenario for an episode of abrupt climate change. We will use a modified version of this scenario to compare two policies with respect to global warming. There is a world-spanning oceanic current which is known to climatologists as the "thermohaline" circulation. The North Atlantic portion, depicted in the figure at the right, is partly responsible for the relative warmth and livability of northwestern Europe. Compared to the frigid wastelands of Labrador, the British Isles are temperate and pleasant to live in, yet they span the same latitudes. If the North Atlantic Current were suddenly to cease warming Europe, then conditions in the British Isles and all of northern Europe would rapidly come to approximate Labrador. Could this really happen? A recent simulation study at the University of Illinois, sponsored by NSF, estimates the probability of this occurrence at 45% between now and 2100, if we continue a policy of doing little or nothing with respect to fossil fuels. Paradoxically, the cause is related to global warming: as the Greenland ice sheet melts, fresh water is released into the North Atlantic Ocean — a process already underway. The dropping salinity disrupts the flow of the North Atlantic Current, and a positive feedback effect locks the change in place. Average temperatures fall by up to 5°C across northern Europe, rainfall is sharply reduced, glaciers expand, crops fail, and millions of people evacuate permanently to warmer climes.

I estimate that the total financial damage to Europe from such a scenario could be from $1 trillion to $40 trillion, depending on the severity of the fall in temperature. It appears that many atmospheric scientists believe that the average temperature drop might be only 2°C, leading to potential damage estimates at the lower end of the range, perhaps $1 trillion. Using a discount rate of 5%, I get a rough estimate of $110 billion for the expected present value of the direct financial loss to Europe caused by a disruption of thermohaline circulation in the North Atlantic Ocean. This is a minimum figure! For completeness we should add in much more for losses felt outside of Europe, and yet more for externalities (defined in TQE 142). The same simulation study also found that a fossil fuel tax ($10 per tonne of carbon) would not eliminate the risk. It would, according to this study, reduce the probability of thermohaline disruption by about two thirds — a very significant reduction, though perhaps not as strong an effect as many tax advocates might wish. Still, we can use this probability to crudely estimate the expected net present value to Europe of a fossil fuel tax: about $40 billion dollars in direct benefit alone, much more if we also take into account indirect benefits to the rest of the world. If the temperature drop is more than 2°C, then the total benefit will climb very rapidly. Here is the critical point: these are concrete present-day numbers that can be compared to the expected net present values of other policy alternatives, to determine which has the best (or least bad) outcome. Without the adjustment for time and uncertainty, it is almost impossible to compare alternatives. ConclusionI hope that I have brought to light the general logic of evaluating the expected present value of uncertain future benefits and losses. With respect to the specific example of thermohaline disruption, if we really believe these calculations — and in reality there is no consensus as yet on this point — then they may become a spur to vigorous action to reduce the drivers of global warming.

Sincerely your Friend, Loren Cobb * It's actually a little more complicated than that. If an uncertain event has a potential benefit X, and there is a different benefit Y that obtains if the event does not occur, then the expected benefit is pX + (1-p)Y, where p is the probability that the event occurs. In the lottery example there is no benefit to losing the lottery (unless you wait 100 years for the ticket to become an antique), so here the expected benefit is just pX.

Readers' CommentsPlease send comments on this or any TQE, at any time. Selected comments will be appended to the appropriate letter as they are received. Please indicate in the subject line the number of the Letter to which you refer! Perhaps a future article will discuss an idea due to Hans-hermann Hoppe, that a people's discount rate is inversely proportional to their level of civilization. The more civilized the society, the lower will be their discount rate. Conversely, anything that increases the discount rate harms civilization. Two examples: eminent domain, estate taxes. — Russ Nelson, St. Lawrence Valley (NY) Friends Meeting. Loren, your explanation of the discount rate and how it is used is an excellent simplification of a rather complex subject. While TQE is perhaps not the place to delve into the theory of cost of capital, your statement that in the business world it is the interest rate for a loan is not true. This completely ignores the not-well-understood fact that all capital has a cost. For any business it is the weighted average of debt and equity capital, based on the percentage of each type of capital employed and the relative costs of each. Determining the cost of equity capital is not a trivial matter, and is of particular importance in regulated industries where the allowed rate of return on capital is based on its cost. Although cost of capital is often equated with rate of return, for any successful business the actual return will be greater than cost. — Dick Bellin.

Loren, it seems to me that the discount rate for economic cost and that for human cost is very different. It is logical that a dollar ten years from now is worth less than a dollar today, since there is a clearly observable and measurable time value of money in the form of real interest rates. But can one say that the value today of a human life ten years from now is less than the value of a human life today? I don't think so. Looked at another way, at a 5% rate, are we willing to say that a single life now is worth 11.5 lives in 50 years? As a Quaker and an ex-archaeologist, I find it hard to say that my life has any greater or lesser value than someone who lived 5000 years ago or who will live 5000 years in the future. If that is the case, if the value of human life has no time element, then the kind of calculations that are dear to the heart of an economist (or an actuary) aren't going to work when we consider the very high possible human cost of environmental destruction. And the implications for policy are quite different. Thank you for another stimulating discussion. — Andrew Tomlinson, Chatham-Summit Monthly Meeting, NJ.

Thank you from an interested African. I find your newsletters very stimulating and its so good to see sensible arguments put forward and seriously debated. As an economist I often feel as if I am the only one hearing the drum of really using the market; that the market could be directed towards the very important goals of increasing the incomes of the poor and at the same time address environmental issues. Having seen the ravages caused by cronyism, even with a very socialist heart, I believe that only the market can work. The disappointment to the world is where the USA is leading these days — apart from its aggression, a free market assessment of the economic policies implemented by your President could not be said to be reflecting the "invisible hand" and are no less self-serving than those of many of the dictators he, and his merry band of kleptocrats, so often decry. When I feel really depressed I envision them, and all (or most) of the African presidents and their entourages on a space ship to Pluto. But I wonder if we will have the gas to send it on its way! — Kay Muir-Leresche (former Zimbabwean). Discounting future events is an extremely useful exercise, and measuring how people discount for potential losses and gains is a delightful exercise coming into more common use in behavioral economics. These techniques are applicable to all kinds of conundrums and dilemmas. For example, folks will often say things like "you can't put a value on a human life." Well, while such an exercise is fraught with ethical and moral inflections, there is nonetheless clearly a "time value" to a human life. This is evidenced with a brief example: Anyone who would claim that there is no "value" difference between being run over by a truck today or ten years from now would be judged a candidate for serious mental health interventions. On the other hand, to apply discounting out past 25 years, much less for 140 years (seven generations today would more likely be 175 or perhaps 210 what with later families and all) will mostly miss the target. Technological changes at today's pace suggest to me that the primary controllable factors affecting human quality of life in 50 years are not even known today and therefore cannot be effectively discounted into these kinds of analysis. Thanks so for your thoughtful presentations and valuable insights. In Joy and Light, — Christopher Viavant, Salt Lake Monthly Meeting.

Found on the Web"I read every issue of Forbes, in order to get an idea of the world-view of the prototypical 'Rich Person' ... For the same reason, but in search of information about a very different world-view, I read The Quaker Economist, and am often astonished at what I find there. Sometimes I agree, sometimes I don't, but I always learn something. Unlike Forbes, it's free." — Ozarque, 8 Jan 2006. Masthead

Copyright © 2006 by Loren Cobb. All rights reserved. Permission is hereby granted for non-commercial reproduction. |

By bringing the impact of future events into the present, suitably discounted for time and uncertainty, we gain the ability to compare policy alternatives and their outcomes. Even so, it would be wise always to bear in mind that these methods still omit any accounting for purely biological losses and disruptions, in all those parts of the biosphere that are not connected to any pricing mechanism.

By bringing the impact of future events into the present, suitably discounted for time and uncertainty, we gain the ability to compare policy alternatives and their outcomes. Even so, it would be wise always to bear in mind that these methods still omit any accounting for purely biological losses and disruptions, in all those parts of the biosphere that are not connected to any pricing mechanism.